For More News And info: Space Coast Daily Uk

news

FBI Warns Chrome Users About New Online Scam: What You Need to Know (2025 Update)

Introduction

The Federal Bureau of Investigation (FBI) has issued an official warning for Google Chrome users in late 2025, highlighting a growing wave of online scams that target unsuspecting internet users through fake browser pop-ups and phishing extensions. This alert comes amid a rise in digital fraud and identity theft cases across the United States and Europe, where cybercriminals are using sophisticated tricks to steal sensitive information.

In this article, we’ll explain what the FBI warning means, how these scams work, and what steps you can take to keep your browser and data safe.

Why the FBI Issued a Warning

According to the FBI’s Internet Crime Complaint Center (IC3), recent investigations revealed that hackers are exploiting Chrome browser notifications and fake updates to trick users into installing malware. These scams usually appear in the form of:

-

Fake “Update Chrome” pop-ups that look identical to Google’s official notifications

-

Malicious Chrome extensions disguised as productivity tools or video downloaders

-

Scam websites prompting users to “verify” their account or “restore access” to Gmail

The FBI emphasized that these fake alerts are not from Google. Once users click the malicious link, hackers gain remote access to their device, allowing them to steal passwords, banking information, and even two-factor authentication codes.

How the Chrome Scam Works

Cybersecurity experts explain that the scam uses social engineering techniques to convince users that their browser needs an urgent update. Here’s how it typically unfolds:

-

You visit a compromised or unsafe website.

-

A pop-up window appears saying “Your Chrome browser is outdated – update now.”

-

Clicking the “Update” button downloads a malicious file or extension.

-

The malware silently runs in the background, logging your keystrokes or capturing saved passwords.

In some cases, victims have also reported screen-locking ransomware attacks, where scammers demand payment to unlock the browser.

FBI’s Official Recommendations for Chrome Users

To help users stay protected, the FBI and cybersecurity experts recommend following these steps:

1. Update Chrome Manually

Never trust random pop-ups. Go to Settings → About Chrome to update your browser directly from Google.

2. Avoid Installing Unknown Extensions

Only download extensions from the official Chrome Web Store, and check user reviews and permissions before installation.

3. Enable Safe Browsing

In Chrome settings, turn on Enhanced Safe Browsing to automatically detect dangerous websites and downloads.

4. Use Antivirus and Two-Factor Authentication (2FA)

Install a trusted antivirus and enable 2FA on important accounts to add an extra layer of security.

5. Stay Informed

Regularly visit the FBI’s official website (fbi.gov) and Google’s security blog to stay updated on the latest scam alerts.

How This Scam Affects the UK and Global Users

While the warning originated in the United States, cybersecurity agencies in the UK, Canada, and Australia have issued similar alerts. Since Chrome holds more than 60% of the global browser market share, such scams can affect millions of users worldwide.

For UK readers, the National Cyber Security Centre (NCSC) has also shared guidelines on identifying fake browser messages and avoiding phishing attempts.

What To Do If You Clicked a Fake Chrome Update

If you think you’ve fallen victim to one of these scams:

-

Disconnect from the internet immediately.

-

Run a full antivirus scan.

-

Change your Google account and banking passwords from a different, clean device.

-

Report the incident to your country’s cybercrime authority or the FBI Internet Crime Complaint Center (ic3.gov).

Final Thoughts

The latest FBI warning for Chrome users serves as an important reminder that even trusted platforms can be exploited by cybercriminals. Always verify browser updates, avoid suspicious links, and keep your software secure.

Online safety depends not just on technology but also on awareness. Stay informed, stay cautious, and help others by sharing this information.

Disclaimer

This article is for informational and educational purposes only. It summarizes details from official FBI and cybersecurity advisories available to the public at the time of writing. Space Coast Daily UK does not claim or represent any official statement from the FBI, Google, or any government agency. Readers are advised to verify all security-related updates directly from official sources such as fbi.gov or google.com before taking any action.

Related Article:

👉 What Is Janitor AI? Features, Use Cases & How To Use It Safely in 2025

👉 Visit Space Coast Daily UK for more tech and cybersecurity updates.

news

UK Digital Economy Transformation: How AI and New Regulations Are Reshaping British Commerce in 2026

Britain’s digital economy stands at an inflection point in 2026, as artificial intelligence integration, regulatory tightening, and shifting consumer behaviors converge to reshape online commerce. From AI-assisted product discovery to new child protection mandates, the landscape facing British retailers and digital platforms has transformed fundamentally, creating both opportunities for innovative local businesses and compliance challenges for established players.

The AI Commerce Revolution: Beyond the Hype

Artificial intelligence has moved from experimental technology to operational necessity in UK digital commerce, though 2026 marks a critical transition from promise to performance measurement. While 2025 saw widespread AI adoption for customer service automation and inventory management, current business imperatives demand demonstrable return on investment rather than speculative future benefits.

The real impact of AI in 2026 is manifesting in the “mid-funnel”—the research and consideration phase of consumer journeys. British shoppers increasingly rely on AI-assisted product discovery tools that aggregate reviews, compare specifications, and personalize recommendations based on individual preferences and constraints. This shift has profound implications for retailer marketing strategies:

Search Optimization Transformation – Traditional SEO focused on keyword density and backlink profiles; AI-assisted discovery prioritizes structured data, semantic relevance, and natural language understanding. Retailers must optimize for conversational queries rather than fragmented keywords.

Review Management Criticality – AI systems weight review sentiment heavily in recommendations, making reputation management essential rather than optional. Fake review detection algorithms have improved, rendering manipulation strategies increasingly risky.

Personalization at Scale – Machine learning enables individualized storefronts presenting different product assortments, pricing, and content to distinct customer segments, raising both opportunity and privacy compliance concerns.

Predictive Inventory – Demand forecasting capabilities reduce stockouts and overstock situations, improving cash flow and customer satisfaction simultaneously.

However, “agentic commerce”—AI systems that autonomously complete purchases based on learned preferences—remains niche in 2026. Consumer trust barriers and regulatory uncertainty limit deployment, though early adopters in subscription services and replenishment categories demonstrate viable models.

Regulatory Tightening: The New Compliance Environment

UK digital commerce faces unprecedented regulatory density as policymakers address concerns about consumer protection, market competition, and social harms. Three major regulatory streams are converging in 2026:

Online Safety Regulations – New rules around child protection require platforms to implement age verification systems and content filtering that significantly increase operational complexity. The Online Safety Bill’s implementation creates compliance costs that disproportionately affect smaller retailers lacking dedicated regulatory affairs capabilities.

Advertising Restrictions – Junk food advertising limitations and targeting restrictions force platforms and advertisers to rethink verification and creative strategies. The traditional model of granular behavioral targeting is giving way to contextual and cohort-based approaches that reduce efficiency but address public health concerns.

Competition Policy – The Digital Markets, Competition and Consumers Act empowers regulators to address platform market power, potentially affecting how major marketplaces treat third-party sellers. British businesses hope these interventions will create fairer competitive environments against dominant global players.

These regulatory developments create particular challenges for small and medium enterprises (SMEs) that lack compliance infrastructure. Industry associations report increasing demand for shared services addressing regulatory requirements, suggesting market evolution toward compliance-as-a-service models.

The Local Business Renaissance: Temu, TikTok, and British SMEs

Paradoxically, the same regulatory and technological shifts threatening established models are creating opportunities for British local businesses. Chinese e-commerce platforms Temu and TikTok Shop have pivoted toward localized strategies that, rather than displacing domestic retailers, are creating new partnership opportunities for UK sellers.

This “localized focus” manifests in several ways:

Platform Partnership Programs – Temu and TikTok have established programs specifically supporting UK-based sellers, providing marketplace infrastructure while leveraging platform traffic acquisition capabilities. British SMEs gain access to national and international customer bases without building independent digital marketing capabilities.

Supply Chain Localization – Regulatory pressures and consumer preferences for shorter supply chains have prompted platforms to prioritize UK-based inventory, reducing delivery times and environmental footprints while supporting domestic businesses.

Content Commerce Integration – TikTok’s social commerce model enables British creators and small businesses to monetize audiences through seamless shopping integrations, democratizing access to e-commerce capabilities previously requiring substantial technical investment.

Quality Positioning – Against ultra-low-cost imports, British businesses are differentiating through quality assurance, sustainability credentials, and local customer service—attributes that resonate with concerned consumers.

Early data suggests these developments are improving fortunes for UK small and medium businesses, particularly in categories where provenance and quality assurance matter. However, success requires digital literacy and adaptive capacity that remain unevenly distributed across the business population.

Cost of Living Crisis: Consumer Behavior Transformation

Persistent inflation and wage stagnation have fundamentally altered British consumer behavior, with implications for digital commerce strategy. The “cost of living crisis” dominates household financial planning, creating both challenges and opportunities for retailers.

Key behavioral shifts include:

Value Consciousness – Consumers engage in extensive comparison shopping, utilizing AI tools and price comparison platforms to identify optimal deals. Brand loyalty has eroded in favor of transaction utility maximization.

Trade-Down Patterns – Premium and luxury categories face demand pressure while value-oriented alternatives gain market share. Private label products and discount platforms experience growth against mainstream brands.

Sustainability Tensions – Environmental concerns remain salient but compete with immediate budget constraints. “Green premium” tolerance has declined, though sustainability credentials influence choices when price parity exists.

Experience Prioritization – Reduced discretionary spending concentrates on experiences rather than goods, affecting digital commerce categories differently. Travel and entertainment booking platforms show resilience against physical goods retail weakness.

Retailers responding successfully to these shifts emphasize transparent value communication, flexible payment options including buy-now-pay-later services, and loyalty program redesigns that emphasize immediate utility over deferred rewards.

Hybrid Work Stabilization: Geographic Demand Redistribution

The normalization of hybrid working arrangements has stabilized following pandemic disruption, creating predictable patterns of geographic demand redistribution. London business leaders confirm that “mixed approach is here to stay,” with implications for digital commerce logistics and marketing.

Research indicates optimal arrangements involve partial office presence rather than fully remote or fully in-person models. “If you spend five days a week working from home, you are engaged but you’re not thriving… if you’re fully returned back to the office, you’re actually both less engaged and less thriving.” This insight suggests hybrid work will persist as the dominant model.

For digital commerce, hybrid work creates:

-

Suburban demand growth for home office equipment, domestic convenience services, and local amenities

-

Urban core weakness in traditional business district retail and service demand

-

Delivery pattern changes as residential deliveries displace office deliveries

-

Marketing timing shifts as consumer attention patterns adapt to flexible schedules

Retailers optimizing for these patterns are reallocating inventory, adjusting delivery network configurations, and recalibrating promotional timing to align with hybrid work lifestyles.

Data Sovereignty and Infrastructure Pressures

The intersection of AI expansion and data-intensive commerce is creating infrastructure pressures with political dimensions. Data center construction has accelerated to support AI applications, generating local opposition over energy consumption, water usage, and land use impacts.

Simultaneously, debates over data sovereignty intensify as businesses and regulators seek control over where and how data is held. Post-Brexit Britain is developing distinct approaches from both EU and US frameworks, creating compliance complexity for international businesses while potentially offering competitive advantages for domestic data infrastructure providers.

These dual trends—centralized computing capacity and decentralized policy control—will feature prominently in UK digital strategy discussions throughout 2026, affecting everything from cloud procurement decisions to AI development location choices.

Skills and Talent: The Digital Capability Gap

Digital commerce transformation requires human capabilities that remain scarce in the UK labor market. The “future of work” discourse emphasizes AI collaboration skills, data literacy, and adaptive learning capacity—competencies that current education and training systems struggle to supply at required scale.

Particular shortages affect:

-

AI implementation specialists who bridge technical and business domains

-

Data governance professionals addressing regulatory compliance requirements

-

Cybersecurity experts protecting increasingly complex digital commerce infrastructure

-

Digital marketing strategists navigating AI-transformed customer acquisition

Immigration policy adjustments post-Brexit have not fully addressed these shortages, while domestic training pipeline expansion requires lead times that extend beyond immediate needs. This capability gap constrains digital commerce transformation velocity and may disadvantage UK businesses against international competitors with deeper talent pools.

Conclusion: Navigating Transformation

The UK digital economy in 2026 presents a complex landscape of technological opportunity, regulatory constraint, and consumer behavioral evolution. Success requires businesses to move beyond experimental AI adoption toward measurable value creation, while navigating compliance environments that increasingly prioritize consumer protection over commercial convenience .

For British SMEs, the localization strategies of major platforms offer unexpected partnership opportunities that may counterbalance competitive pressures from global giants. However, realizing these benefits requires digital literacy and adaptive capacity investments that many businesses have deferred .

As the year progresses, the interaction between AI capabilities, regulatory frameworks, and economic conditions will determine whether 2026 becomes remembered as a year of British digital commerce renewal or merely another chapter in ongoing competitive struggle. The stakes for business strategy, employment, and economic prosperity could not be higher.

news

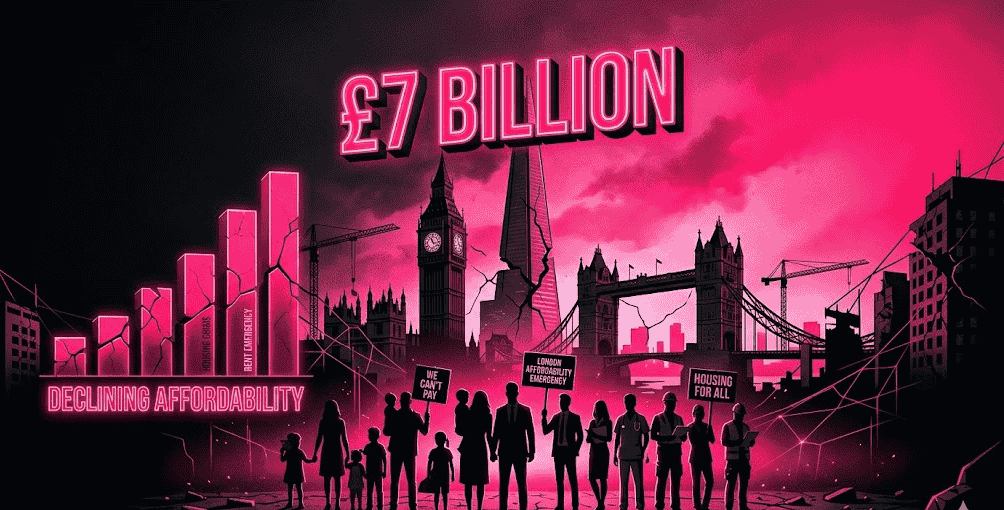

UK Housing Crisis Deepens: How London’s Affordability Crisis is Costing the Economy £7 Billion and Shaping the 2026 Political Landscape

The United Kingdom faces what economists and policymakers increasingly characterize as a generational housing crisis, with London’s affordability challenges alone estimated to cost the national economy over £7 billion in lost output annually. As the May 2026 local elections approach, housing has emerged as the defining political issue, with the Government and Mayor’s emergency housebuilding measures representing merely the opening phase of what must become a sustained national effort.

The Scale of the Crisis: By the Numbers

Housing affordability in London has deteriorated to levels unseen in modern British history. The ratio of median house prices to median earnings has reached extremes that effectively exclude younger generations from homeownership, while rental costs consume unprecedented shares of household income. Research indicates that a mere 1% improvement in London housing affordability would generate over £7 billion in additional economic output—a figure that illustrates both the current drag on prosperity and the potential gains from effective intervention.

The crisis extends far beyond London, affecting major urban centers across England, Scotland, and Wales. However, the capital’s concentration of economic opportunity makes its housing shortage particularly consequential for national productivity. When skilled workers cannot afford to live within reasonable commuting distance of employment centers, labor market matching suffers, innovation ecosystems weaken, and economic dynamism declines.

Economic Consequences: Beyond Individual Hardship

The housing crisis manifests as individual hardship—overcrowding, insecurity, and the psychological toll of precarious tenure—but its economic consequences radiate throughout the national economy:

Recruitment and Retention Challenges – Employers across sectors report difficulty attracting talent to London and other high-cost areas. This “talent drain” particularly affects public services, including the National Health Service and education, where salary scales lag far behind housing costs. The resulting staffing shortages reduce service quality while increasing reliance on expensive agency arrangements.

Productivity Impacts – Long-distance commuting, often necessitated by housing cost differentials, reduces worker productivity through fatigue and time loss. The Office for National Statistics has documented correlations between commuting duration and output per hour, suggesting significant macroeconomic costs from current settlement patterns.

Fiscal Pressures – Housing benefit expenditures have grown substantially, reflecting private rental sector inflation. Meanwhile, stamp duty receipts fluctuate with market volatility, creating uncertainty in public finances. The combination of rising expenditure and unstable revenue complicates fiscal planning at both national and local levels.

Wealth Inequality Amplification – Homeownership has become the primary determinant of lifetime wealth accumulation in Britain. Those fortunate enough to purchase property before the sustained price escalation of recent decades have captured enormous capital gains, while younger cohorts face permanent exclusion from this wealth-building mechanism. This intergenerational inequity threatens social cohesion and political stability.

Government Response: Emergency Measures and Their Limitations

The Government and Mayor of London have introduced emergency housebuilding measures that mark “a step in the right direction” according to business leaders, yet significant obstacles remain before these policies translate into actual construction.

Current initiatives include:

-

Planning system reform to accelerate approval processes for suitable developments

-

Public land release for housing construction, particularly on brownfield sites

-

Affordable housing funding increases, though critics argue these remain inadequate to demand

-

Rent stabilization measures in the private rental sector

-

First-time buyer support schemes including shared ownership and help-to-buy variations

However, implementation challenges persist. Regulatory complexity continues to delay projects even after planning permission is granted. Construction industry capacity constraints limit the pace at which additional demand can be translated into completed homes. Infrastructure requirements—transport, schools, healthcare facilities—often lag housing development, creating unsustainable communities.

The May 2026 Elections: Housing as Political Fault Line

Local elections scheduled for May 2026 are shaping up as a referendum on housing policy, with political analysts describing unprecedented uncertainty about outcomes. “I’ve never known London to be so uncertain about what the result of a set of local elections will be as it is now,” notes one veteran observer, suggesting that “the public is increasingly open to more radical policy shifts than are immediately obvious”.

The political landscape reveals fragmentation rather than consolidation around established approaches:

Conservative Positioning – Emphasizing homeownership expansion through market mechanisms and planning deregulation, while facing skepticism about implementation credibility given previous governments’ records.

Labour Proposals – Focusing on social housing investment and tenant protections, with detailed policy development constrained by fiscal caution and concerns about alienating middle-class homeowners.

Liberal Democrat Niche – Advocating for community-led development and environmental sustainability in construction, appealing to educated urban professionals but struggling for working-class support.

Green Party Influence – Pushing for zero-carbon housing standards and densification over greenfield development, gaining traction among younger voters but facing resistance in suburban areas.

Reform UK Disruption – Channeling frustration with mainstream parties’ perceived failures, though specific housing policies remain underdeveloped.

This fragmentation suggests that no single party is likely to achieve decisive mandates, potentially necessitating coalition arrangements that could either accelerate innovative solutions or produce policy paralysis.

Regional Variations: Beyond the Capital

While London dominates national housing discourse, distinctive challenges affect other regions:

Southeast England – Commuter belt communities face London spillover demand, pricing out local workers in essential services while creating “dormitory towns” with limited economic vitality.

Northern Powerhouse Cities – Manchester, Leeds, and Newcastle experience gentrification pressures in central areas while peripheral neighborhoods suffer from abandonment and dereliction. The “levelling up” agenda has yet to produce consistent housing improvement.

Coastal and Rural Areas – Second-home purchases and short-term rental conversions for tourism have displaced local populations in desirable locations, creating community tensions and service provision challenges.

Devolved Administrations – Scotland and Wales pursue distinct policy approaches, with Scotland’s rent control measures providing natural experiments for evaluation, while Wales emphasizes cooperative and community housing models.

These variations complicate national policy formulation, as interventions effective in London may prove inappropriate or counterproductive elsewhere.

Construction Industry Capacity: The Bottleneck

Even with optimal policy frameworks, housing supply expansion faces fundamental constraints in construction sector capacity. The industry has shed skilled workers following previous boom-bust cycles, while apprenticeship programs have failed to replenish the workforce. Brexit-related immigration changes have further reduced labor supply, particularly in specialized trades.

Material cost volatility, driven by global supply chain disruptions and energy price fluctuations, adds uncertainty to development economics. Housebuilders report difficulty securing construction financing for speculative developments, while the planning permission pipeline remains clogged with approved but unbuilt projects.

Addressing these supply-side constraints requires coordinated action across education policy, immigration rules, financial regulation, and industrial strategy—a complexity that challenges existing governmental structures.

Innovative Solutions: Emerging Models

Amid policy frustration, innovative approaches are emerging from local authorities, housing associations, and private developers:

Modular Construction – Factory-built housing components promise quality control and speed advantages, though adoption remains limited by financing conventions and planning system inertia.

Community Land Trusts – Non-profit mechanisms separating land ownership from building ownership preserve long-term affordability while enabling individual equity accumulation.

Co-Living Developments – Purpose-designed shared housing addresses isolation while reducing individual space requirements, particularly appealing to young professionals.

Adaptive Reuse – Converting obsolete commercial buildings—particularly post-pandemic office space—into residential use addresses both housing supply and urban vitality challenges.

Public-Private Partnerships – Risk-sharing arrangements that accelerate infrastructure provision while enabling private development, though these require careful governance to protect public interests.

These innovations offer proof-of-concept for scaled solutions, yet require supportive policy environments and patient capital to achieve transformative impact.

Conclusion: The Stakes for 2026 and Beyond

The UK housing crisis represents more than a policy challenge—it tests the capacity of democratic institutions to address structural problems that have developed over decades. Success in 2026 would demonstrate that coordinated government action can overcome market failures and deliver broadly shared prosperity. Failure, conversely, risks entrenching intergenerational inequality and undermining economic competitiveness.

For London specifically, the £7 billion annual cost of current dysfunction provides both a measure of urgency and a benchmark for evaluating intervention effectiveness. As the May elections approach, voters will determine whether established approaches merit continuation or whether the “growing feeling… that real genuine change needs to come” translates into political mandates for transformative action .

The coming months will prove decisive in determining whether 2026 becomes remembered as the year Britain began solving its housing crisis or merely another milestone in its deepening.

news

Global Trade Reaches $35 Trillion Milestone: 10 Critical Trends Reshaping International Commerce in 2026

International commerce has achieved an unprecedented milestone, with global trade exceeding $35 trillion for the first time in recorded history following a remarkable 7% growth surge in 2025. Yet as 2026 unfolds, this record-breaking performance faces mounting headwinds that promise to fundamentally reshape how nations and businesses engage in cross-border exchange.

The $35 Trillion Achievement: Context and Significance

The record trade figures represent more than statistical milestones—they reflect deep structural changes in global economic organization. Developing economies have captured an increasing share of this growth, while digital services and green technologies have emerged as the fastest-expanding trade categories. This expansion has lifted millions from poverty while creating new dependencies and vulnerabilities in integrated supply chains.

However, preliminary data suggests 2026 will bring slower growth as geopolitical tensions, protectionist policies, and structural adjustments temper the previous year’s momentum. UN Trade and Development projections indicate that while trade will remain positive, the pace will decelerate significantly, creating a more challenging environment for export-dependent economies.

Geopolitical Fragmentation Reshapes Trade Maps

The most significant force affecting global commerce in 2026 is the accelerating fragmentation of trade relationships along geopolitical lines. Major economies are increasingly prioritizing security and strategic autonomy over efficiency, resulting in the reconfiguration of supply chains that have defined globalization for three decades.

The United States has continued implementing tariffs as protectionist tools, with average global tariffs rising unevenly across sectors. These measures, while designed to protect domestic industries, have created substantial uncertainty that discourages investment and long-term planning. Smaller, less diversified economies face particular exposure, with limited capacity to absorb higher costs or redirect exports to alternative markets.

China’s export controls on critical minerals and rare earth elements have prompted allied nations to develop alternative supply frameworks, including the proposed “Pax Silica” initiative aimed at securing technology supply resilience across partner countries. These developments signal a permanent shift from efficiency-driven globalization to security-conscious trade regionalization.

Value Chain Reconfiguration Creates Winners and Losers

Nearly two-thirds of global trade occurs within value chains, making their reconfiguration the single most important structural trend in international commerce. Companies are moving away from cost-driven offshoring toward risk management approaches that prioritize supply security over marginal cost savings.

This shift is driving:

-

Supplier diversification across multiple geographies to reduce single-point-of-failure risks

-

Production relocation closer to end markets, increasing resilience but potentially reducing efficiency

-

Vertical integration as firms seek to control more of their supply chains to secure critical inputs

For developing economies, these trends create divergent outcomes. Countries with strong infrastructure, skilled workforces, and stable policy environments stand to attract significant new investment. Conversely, peripheral economies risk marginalization unless they rapidly upgrade logistics capabilities and improve investment climates.

The Digital Trade Revolution Accelerates

Services trade, particularly digitally deliverable services, continues expanding faster than goods trade. Cross-border data flows now underpin an increasing share of economic value, creating both opportunities for service-exporting nations and regulatory challenges for data governance.

Artificial intelligence is emerging as a critical factor in trade competitiveness. Nations are pursuing “sovereign AI” strategies to ensure economic security and guard against external technological shocks. This technological nationalism threatens to create new barriers in digital trade even as the underlying connectivity expands.

The World Trade Organization’s 14th ministerial conference, scheduled for Yaoundé, will address digital trade frameworks amid rising unilateral measures and growing use of trade restrictions. Outcomes will determine whether global trade rules adapt to digital realities or fragment further along national lines.

Green Transition Transforms Commodity Markets

Environmental priorities are increasingly shaping trade patterns as climate commitments move into implementation phases. Enhanced pledges by 113 countries could reduce global emissions by approximately 12% by 2035, creating massive demand shifts in energy and industrial markets.

Clean-energy technology markets are projected to reach $640 billion annually by 2030, accelerating trade in green goods and services. However, this transition is creating new trade tensions through:

-

Carbon pricing and border adjustments, including the European Union’s carbon border mechanism implemented in 2026

-

Clean-energy industrial policies that reshape market access and competitiveness

-

Critical mineral supply constraints as demand for battery materials outpaces supply growth

Developing countries face particular challenges in adapting to these environmental standards, requiring access to green finance, technology transfer, and technical assistance to maintain market access.

Critical Minerals Face Supply Crunch

By late 2025, prices of key clean-energy minerals were trading 18% to 39% below their 2021-22 peaks, reflecting temporary oversupply and slower battery demand growth. However, this price relief masks structural supply risks that will intensify through 2026.

Mining investment growth has slowed dramatically—from 30% in 2022 to just 5% in 2024—while financing focuses on near-mine expansion rather than new greenfield development. Export controls have tightened in major producing regions, including cobalt restrictions in the Democratic Republic of Congo and rare-earth controls in China. These developments suggest looming supply constraints that could derail clean-energy transitions and trigger renewed price volatility.

Agricultural Trade Under Stress

Food and agricultural products account for approximately one-third of commodity exports, with food products representing nearly 87% of this total. Many developing countries remain import-dependent for basic nutritional requirements, making agricultural trade openness a critical food security issue.

Current stressors include:

-

Conflict-related disruptions in major grain-producing and exporting regions

-

Extreme weather events reducing yields and increasing price volatility

-

Fertilizer price surges that raise production costs and threaten farmer solvency

-

Trade restriction cascades as food-insecure nations prioritize domestic availability

The intersection of these factors creates significant vulnerability for import-dependent developing countries with limited fiscal buffers to absorb price spikes.

Regulatory Proliferation Raises Compliance Costs

Since 2020, approximately 18,000 discriminatory trade measures have been introduced globally. Technical regulations and sanitary standards now affect roughly two-thirds of world trade, creating compliance burdens that fall disproportionately on smaller exporters and lower-income economies.

2026 is expected to see further expansion of non-tariff measures addressing:

-

Security and industrial policy concerns, including strategic trade controls

-

Environmental standards, such as deforestation-related import requirements

-

Social and public health standards, adding new compliance dimensions

While these measures often address legitimate objectives, their cumulative impact threatens to exclude developing economies from premium markets unless flexible implementation and targeted assistance accompany regulatory expansion.

Services Trade Liberalization Stalls

Despite digital expansion, traditional services trade liberalization has stalled amid rising nationalism in professional services, transportation, and financial services. Regulatory barriers to services trade often exceed those affecting goods, yet receive less attention in trade negotiations.

The services sector’s growing share of employment and output makes this stagnation economically significant. Countries with competitive services sectors—particularly in business process outsourcing, software development, and creative industries—face unrealized export potential due to restrictive foreign investment and professional licensing regimes.

Regional Trade Agreements Proliferate

As multilateral negotiations struggle, regional and bilateral trade agreements continue multiplying. These arrangements offer deeper integration than global frameworks but risk creating complex overlapping obligations that increase transaction costs for businesses operating across multiple regions.

Africa’s Lobito Corridor initiative, connecting mineral-rich interior regions to Atlantic ports, exemplifies infrastructure-focused regional integration that addresses historical connectivity deficits. Similar initiatives across Southeast Asia and Latin America suggest regionalization may prove more durable than globalization in the current environment.

Trade Finance Gaps Threaten Recovery

Trade finance availability remains constrained, particularly for small and medium enterprises and transactions involving higher-risk jurisdictions. The withdrawal of correspondent banking relationships from certain regions has created “financial deserts” where legitimate trade cannot obtain necessary payment and credit instruments.

Multilateral development banks have expanded trade finance programs, but gaps persist. Digital trade finance solutions offer potential breakthroughs, but regulatory acceptance and interoperability standards remain underdeveloped.

Conclusion: Navigating Fragmentation

The $35 trillion trade milestone represents both achievement and vulnerability. Record volumes demonstrate the resilience of international commerce, yet the trends shaping 2026 suggest increasing friction and fragmentation. Success in this environment requires businesses and policymakers to prioritize resilience over efficiency, diversification over concentration, and adaptive capacity over rigid optimization.

For developing economies, the imperative is clear: upgrade infrastructure, develop skills, improve governance, and strengthen regional integration to capture opportunities in reconfigured value chains. For established trading powers, the challenge involves managing geopolitical competition without collapsing into mutually destructive protectionism. The coming years will determine whether international trade continues lifting global prosperity or fragments into competing blocs with diminished collective welfare.

For More News And info: Space Coast Daily Uk,

-

news2 days ago

UK Housing Crisis Deepens: How London’s Affordability Crisis is Costing the Economy £7 Billion and Shaping the 2026 Political Landscape

-

AI & Innovation2 days ago

AI & Innovation2 days agoUN Launches First-Ever Global AI Panel: How Artificial Intelligence is Reshaping Governance, Economy, and Society in 2026

-

news2 days ago

UK Digital Economy Transformation: How AI and New Regulations Are Reshaping British Commerce in 2026

-

news2 weeks ago

news2 weeks agoThe Iran-Israel Military Confrontation of 2026: A Comprehensive Strategic Analysis